Gross margin and contribution margin

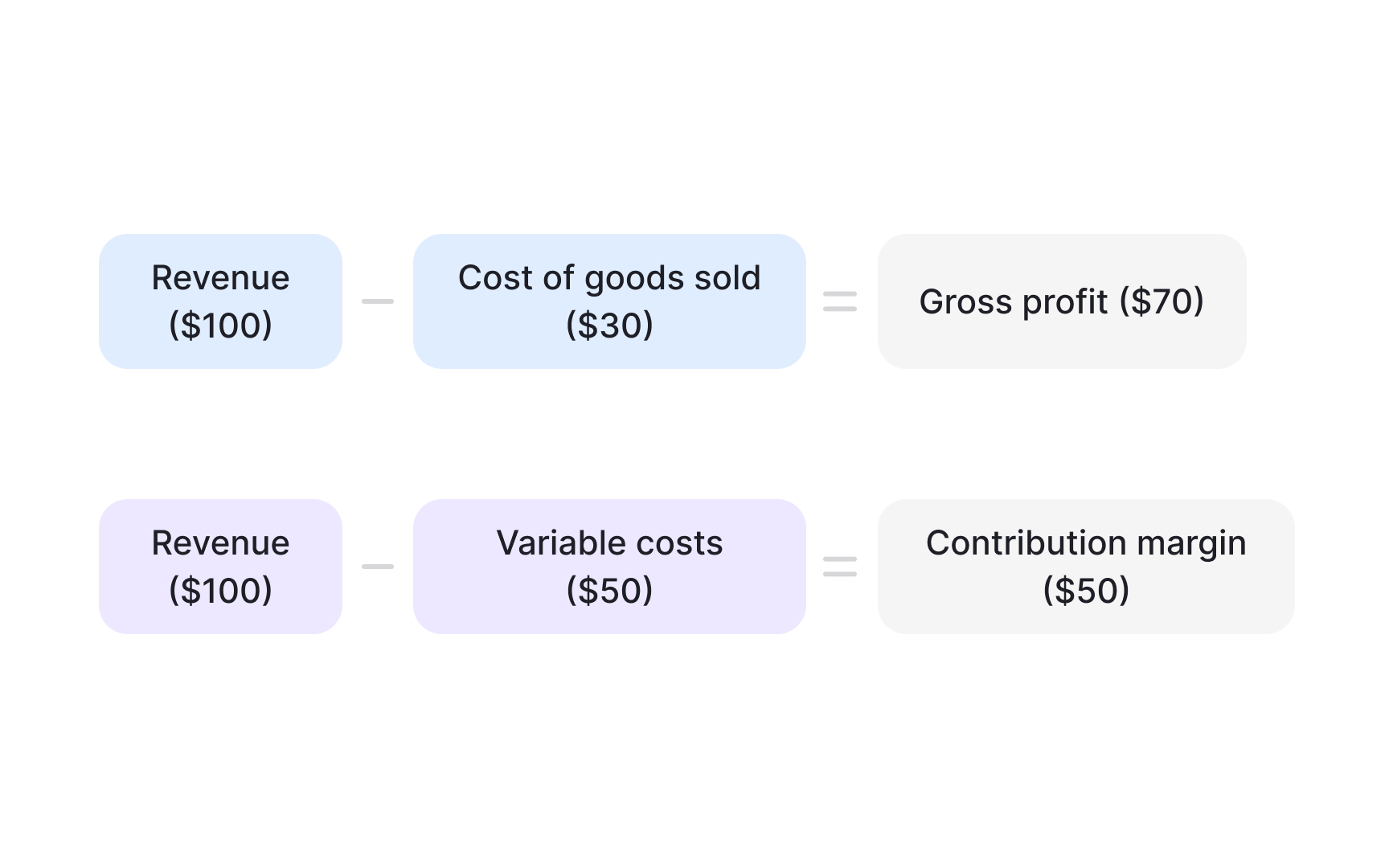

Gross margin shows how much money remains after subtracting the direct costs of making or delivering a product. It is calculated by dividing gross profit by total revenue. For example, a 70% gross margin means that for every $100 in sales, $70 stays after covering direct costs such as materials or hosting. Software products usually have high gross margins because producing an extra copy costs almost nothing (although hosting infrastructure costs can increase with a large increase in users). Physical products tend to have lower gross margins due to manufacturing, shipping, and storage costs.

Contribution margin goes deeper by subtracting all variable costs, such as transaction fees, packaging, or commissions, to show how much profit is left to cover fixed costs like rent, salaries, or software licenses. This metric helps compare the profitability of individual products or features. Products with a negative contribution margin lose money on every sale and should be adjusted or removed. On the other hand, products with strong contribution margins can fund fixed expenses and support business growth.

The key difference is that gross margin gives a broad view of overall profitability, while contribution margin reveals which products or features truly add profit after variable costs.